AMC Networks (NASDAQ:AMCX) is best known for ”The Walking Dead”, which was the highest-rated series in cable history. The unusual nature of the series and its success illuminate the value proposition of AMC Networks within the larger entertainment industry.

In essence, AMC delivers the spice on top of the main course of cable and streaming bundles. Using spice to describe AMC is both a metaphor and a literal depiction. Before turning to the spice, the following section provides an overview of the company’s brands, including their reach. It was compiled from AMC’s 2022 annual report, as are the tables herein, excluding consensus estimates data.

For those familiar with the company, feel free to skip to the next section.

Overview of Brands

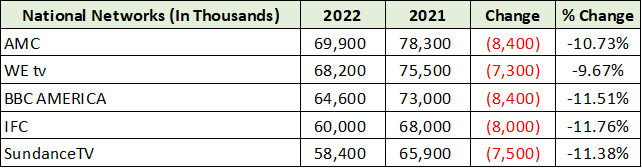

AMC operates five national programming networks which combine original and licensed content:

- AMC: Reaches 70 million Nielson subscribers with some of the most popular and acclaimed dramas on television such as “The Walking Dead” franchise, “Better Call Saul”, and Anne Rice’s “Interview with the Vampire” (the #1 new drama on ad-supported cable in 2022).

- WE tv: Reaches 68 million Nielson subscribers offering targeted content. For example, it is the top US cable network for African American women on Friday nights.

- BBC AMERICA: Reaches 65 million Nielson subscribers and is a joint venture between AMC Networks and BBC Studios.

- IFC: Reaches 60 million Nielson subscribers and offers offbeat, unexpected content with a focus on comedies.

- SundanceTV: Reaches 58 million Nielson subscribers and was founded by Robert Redford with a mission to celebrate creativity and distinctive storytelling through unique voices and narratives. The brand focuses on original scripted programming and true-crime documentaries.

Global streaming services:

- AMC+: The Company’s premium streaming bundle featuring an extensive lineup of programming from AMC, BBC America, IFC, and SundanceTV along with full access to the company’s targeted streaming services: Shudder, Sundance Now and IFC Films Unlimited.

- Acorn TV: North America’s largest streaming service specializing in British and international television with a wide range of genres.

- Shudder: Horror, thrillers, and the supernatural genres. Hollywood favorites, cult classics, original series and critically acclaimed new genre films.

- Sundance Now: Offers cross-genre escapism for viewers seeking fresh perspectives, thought-provoking experiences and transportive journeys to far-off places.

- ALLBLK: Focused on Black content from Black storytellers. The wide range of content spans across genres and generations.

- HIDIVE: An anime-focused streaming service offering a library of television series, movies, and original video animations.

Other operations:

- AMC Studios: In-house production and distribution.

- IFC Films: Film distribution for independent films under two labels, IFC Films and IFC Midnight.

- AMC Networks International: 110 countries and territories. Programmed for local audiences and language. Wide range of genres.

- AMC Networks Broadcasting & Technology: A full-service network programming feed origination and distribution company.

The Spice

What you will notice when reviewing AMC’s brands is the unique and targeted nature of its content (the spice). This is in contrast to industry leaders such as Amazon, Netflix, Comcast, and Disney, which offer broad-based, deep content libraries (the main course). The key takeaway from this industry dynamic is that AMC Networks perfectly complements all of the major content delivery platforms.

The complementary nature of AMC’s content remains the same regardless of the delivery platform, whether a streaming or a cable bundle. Adding spice to a streaming or cable bundle serves a crucial business objective for the large content distribution platforms, subscriber retention. AMC is a uniquely positioned partner for reducing customer churn on large streaming platforms.

Vision

In sharing his vision for the company on the 2022 year-end earnings call, Interim Executive Chairman James L. Dolan stated that the company would follow the industry leaders. The statement appears to contain little in the way of vision. Upon reflection, and in context of AMC offering the spice, the vision offers a viable pathway to success for AMC.

AMC is simply too small to compete with the industry-leading content distribution platforms. For reference, the company’s market value is near $750 million in comparison to the industry leaders whose value is in the $150 billion to $1 trillion plus range. On the content front, AMC’s budget is expected to normalize in the $1 billion per year area. Netflix’s content spend has averaged over $17 billion over the past two years.

Furthermore, the industry leaders are AMC’s distribution partners with whom AMC has long-standing relationships. The five national programming networks summarized above display AMC’s reach with its traditional cable bundle partners, at 70 million households. As can be seen in the following table from the 2022 annual report, this channel remains in a structural decline.

Created by Brian Kapp, stoxdox

As discussed in “Comcast is riding the information wave,” the above declines follow the cord-cutting tsunami of over 25 million households between 2016 and 2021.

While continued cord-cutting is to be expected, from a content perspective there is little difference between a streaming package and a cable bundle. The primary difference is one of customer choice. Using Dolan’s description from the year-end earnings call, this difference translates into AMC becoming more of a retailer of content rather than a content wholesaler.

In other words, the company will increasingly engage with the end consumer directly rather than solely through distribution partners. What is clear from the cord-cutting tsunami is that consumers are increasingly dissatisfied with the value proposition on offer from today’s cable bundles (content and pricing).

Recall that AMC offers the spice rather than the main course of content bundles. The leading news and media brands supply much of the main course of cable bundles. Given the long-standing trend of viewer stagnation and decline across the legacy media brands, the cord-cutting tsunami is likely a result of the value on offer from the main course rather than the spice.

Streaming

Given that AMC’s content is broadly available in cable bundles and streaming services, the company has been reasonably successful in attracting direct streaming customers. As of the end of 2022, AMC had 11.8 million direct streaming subscribers and generated streaming revenue of just over $500 million in 2022. This represents a 35% growth rate over 2021.

The flagship streaming service, AMC+, is available to subscribers through its direct-to-consumer app, MVPDs (cable, satellite etc.), virtual MVPDs, and streaming platforms such as Amazon Prime Video Channels, Apple TV Channels, and The Roku Channel. The company is also conducting packaging tests for AMC+ with leading network partners, such as Verizon.

Looking to 2023, AMC did not provide guidance for the number of streaming customers it expects to achieve by year end. This is likely the result of having little visibility. On the earnings call, Dolan referred to current attempts at content monetization in the entertainment industry as failing. The company did state that it expects streaming subscriber growth to moderate from 2022’s rate.

Fundamentals

Looking at direct-to-consumer streaming, AMC is at a distinct disadvantage compared to its larger competitors (the spice versus the main course). The disadvantage from a standalone streaming perspective relates to AMC’s relatively small owned-content library. From the 2022 annual report:

The majority of the content on our programming networks and streaming services consists of films, episodic series and specials that we acquire pursuant to rights agreements… AMC’s film library consists of films that are licensed under long-term contracts with major studios such as Twentieth Century Fox, Warner Bros., Sony, MGM, NBC Universal, Paramount and Buena Vista.

As all major content owners are now streaming directly to end consumers, the value to AMC of licensing such third-party content is diluted. While this presents a major risk to AMC’s value proposition, it also represents a substantial opportunity. Meaning, it is an opportunity for AMC to be more strategic with its content creation, selection, and licensing.

Balance Sheet

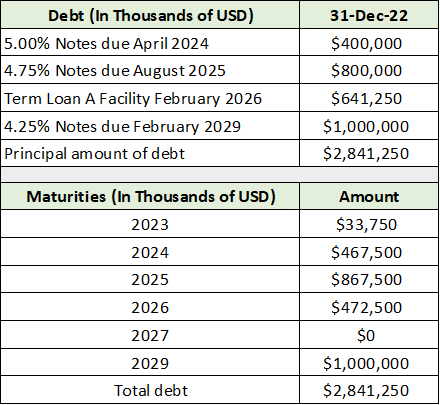

Given the heightened uncertainty, AMC’s financial position takes center stage. It is here that market concerns are the greatest. The following table displays the company’s debt levels and maturities, which illuminate the primary near-term risk facing AMC shareholders.

Created by Brian Kapp, stoxdox

There is concern as to the terms on which AMC can refinance its near-term debt maturities in 2024 and 2025. While not an immediate threat, the 5% and 4.75% notes maturing in 2024 and 2025 will likely face substantially higher rates if successfully refinanced.

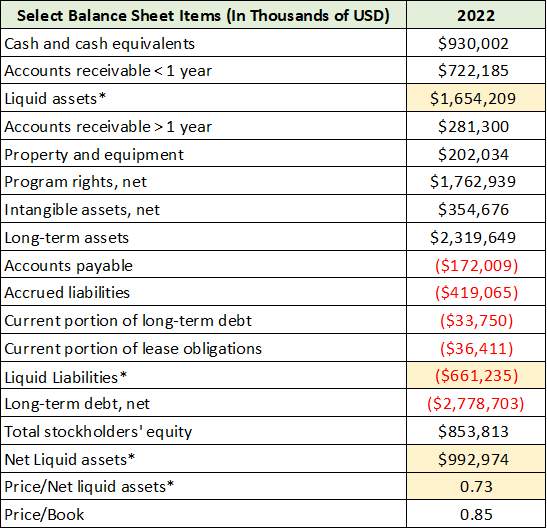

The following table displays select balance sheet items. I have highlighted in yellow my calculations, while the remaining cells are direct line items from the balance sheet.

Created by Brian Kapp, stoxdox

My estimates of cash-like assets and cash-like liabilities result in a net liquid asset position of just under $1 billion. In addition, AMC has access to an undrawn credit line of $500 million.

The company is well positioned to deal with the 2024 debt maturity. While 2025’s debt maturity could create stress, the company has a history of free cash flow generation. As a result, the $1.5 billion liquidity position may be enhanced over the interim. On the 2022 earnings call, management indicated that an annual free cash flow baseline in the range of $185 to $205 million is their current expectation.

At this level of free cash flow generation, the company could have an additional $400 million available around the time of the 2025 maturity. If achieved, free cash flow and the $500 million undrawn credit line could manage the 2025 maturity.

A final note regarding AMC’s debt, the company has debt covenants which could present a risk if business conditions deteriorate significantly from 2022’s results. The company must maintain a ratio of adjusted operating income to net debt of 5x or less and an adjusted operating income to interest expense ratio of 2.5x or greater. The adjusted operating income ratios are roughly 2.75x net debt and 5.11x interest expense today.

While AMC is comfortably within the debt covenant restrictions today, a significant deterioration in business conditions could introduce covenant risk, though it appears unlikely.

Consensus Estimates

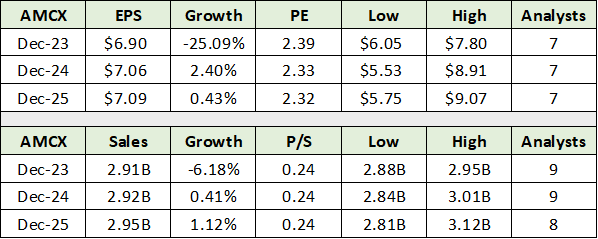

Turning to market expectations, consensus analyst estimates do not reflect a material deterioration in AMC’s business into mid-decade. Instead, analysts expect AMC to stagnate near its 2022 results. The following table displays consensus earnings estimates (top) and consensus sales estimates (bottom) for the next three years. The sales estimates reflect the expectation for stagnation.

Source: Seeking Alpha. Created by Brian Kapp, stoxdox

Notice in the upper section of the table that the company is trading at 2.4x the 2023 consensus earnings estimate. Such a deeply-discounted valuation is clearly unusual. It suggests that the market is not just pricing in earnings misses but the potential for financial stress. Using the lowest analyst estimates, the valuation is only 3x earnings estimates through 2025.

What is most interesting in respect to consensus estimates and AMC’s extraordinarily low valuation is the tight range of sales estimates through 2025 (Low-High columns). The low and high sales estimates have a maximum deviation from the consensus of -5% to +6% in 2025. For 2023, the low to high deviation from the consensus is -1% to +1%. There is no sales uncertainty evident in analyst estimates.

With AMC Networks trading at 2.4x consensus estimates through mid-decade, the market is pricing in a material and sustainable impairment to AMC’s equity value. The distressed valuation at 2.4x consensus estimates juxtaposed against the stability of consensus sales estimates illuminates the essence of the AMC investment case.

Will AMC Survive?

If in fact the industry is failing to profitably monetize content, the current phase change in content distribution could leave many casualties. It is possible that AMC’s equity could be one such casualty.

My take on the content monetization problem is that it is a question of the content itself. If the content is desired, success is within one’s control. Successful packaging and price points are an operational problem, and thus solvable.

As the continuing cord-cutting tsunami attests, cable bundles are failing in today’s market. Though they remain highly profitable businesses and are far from dead, it is fair to say that the monetization strategy is generally failing. The failure reflects the content itself rather than consumers’ willingness to pay the cable bundle price point per se.

The question is whether AMC delivers content that is desired and at what price. If at the cable bundle price, then certainly AMC’s content will not be desired. Using a back of the napkin approach, what if AMC can successfully deliver at a $5/month value proposition? If we ignore the monetization channel itself, and assume the content is ultimately desired and monetized at $5/month, AMC could have a bright future.

For example, Netflix has 231 million subscribers. At $5/month this would translate into $14 billion of revenue. If in the 70 million cable customer range, the revenue would then be in the $4 billion range. The growth potential for each of these sales levels is 366% and 33%, respectively.

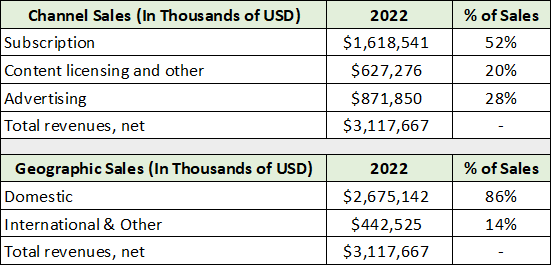

In addition to the above potential, AMC has material advertising and licensing revenue. A breakdown of the company’s sales is provided in the following table. Note that the company has a long growth runway in international markets while possessing three monetization vectors across all markets.

Created by Brian Kapp, stoxdox

Technicals

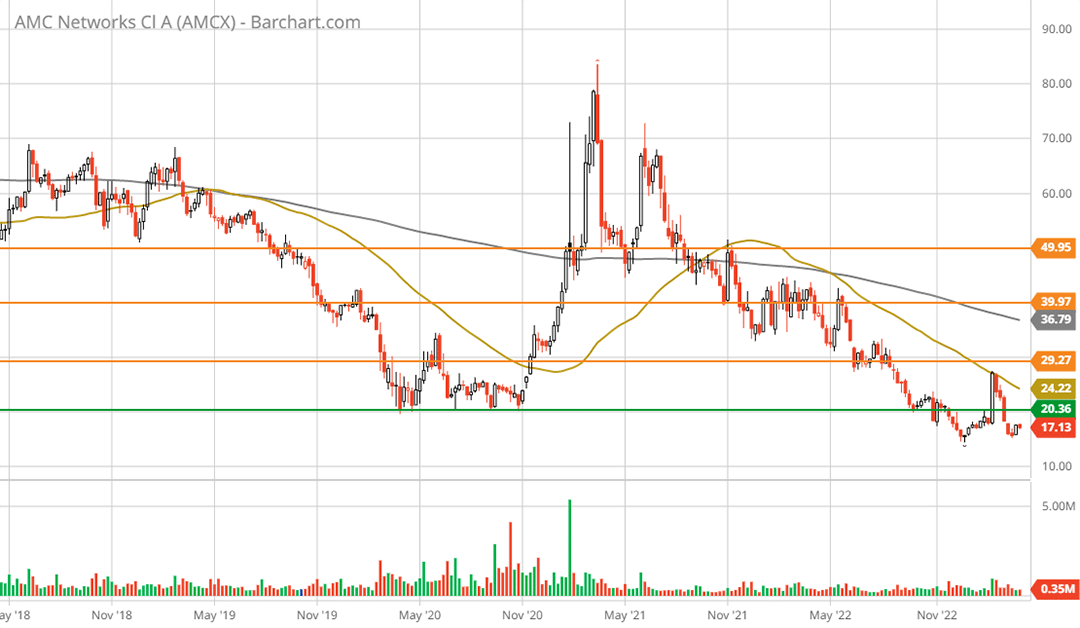

The technical backdrop mirrors the fundamental asymmetry. The following 5-year weekly chart captures the key support level (the green line) and resistance levels (orange lines) for AMC. Note that the resistance levels represent the upside price targets.

AMC Networks 5-year weekly chart. Created by Brian Kapp using a chart from Barchart.com

AMC is currently testing its only visible support and is at a new all-time low since its IPO in June 2011. Given the deep valuation discount, this region should offer strong support. The upside potential to each of the three resistance levels is 76% ($30), 135% ($40), and 194% ($50).

Summary

From a portfolio perspective, whether AMC Networks survives or thrives, the risk/reward asymmetry is decidedly skewed to the upside. The positive risk/reward rating is bolstered by AMC’s strong liquidity profile, which appears sufficient to successfully manage its debt maturities into mid-decade. While there is a possibility of failure in the longer term, it appears to be highly unlikely in the foreseeable future.

Price as of this report: $17.13

AMC Networks Investor Relations